Outsourcing Customer Onboarding for Digital Banks presents a critical operational capability for financial institutions struggling with scale and compliance across diverse customer segments. Managing the intricate journey from initial KYC verification to full service activation often results in high drop-off rates, directly impacting revenue and market share. This article delineates a strategic framework for leveraging external expertise to optimize the entire customer acquisition lifecycle, enhancing both efficiency and regulatory adherence through a structured onboarding approach.

Customer onboarding outsourcing for digital banks involves delegating the end-to-end process of new client acquisition, identity verification, and initial service setup to specialized third-party providers, ensuring compliance and operational scalability.

In high-volume digital banking environments, the operational burden of customer onboarding can strain internal resources, particularly as regulatory landscapes become more complex. External partners offer specialized platforms and expertise, designed to absorb this volume while maintaining stringent compliance standards. This approach allows digital banks to focus on core product innovation and customer engagement, rather than the intricate mechanics of identity verification and account provisioning.

Successful implementation requires a clear understanding of system architecture, robust governance frameworks, and a phased deployment strategy. The objective is to achieve demonstrable improvements in customer conversion rates and operational cost reduction, crucial metrics in a competitive market.

Strategic Imperatives for Enhanced Digital Onboarding

The imperative for seamless, secure, and compliant onboarding is non-negotiable for digital banks. Manual processes are prone to human error and significantly extend time-to-activation, contributing to customer frustration and abandonment. Adopting an outsourced model provides access to advanced technology stacks and specialized personnel without substantial upfront capital expenditure.

Consider the typical digital bank operating model where rapid expansion dictates agility. An outsourced solution can scale instantaneously to meet fluctuating demand, from peak promotional periods to organic growth surges, without requiring internal headcount adjustments or infrastructure upgrades. This elasticity is fundamental to maintaining a competitive edge and capturing new market segments efficiently.

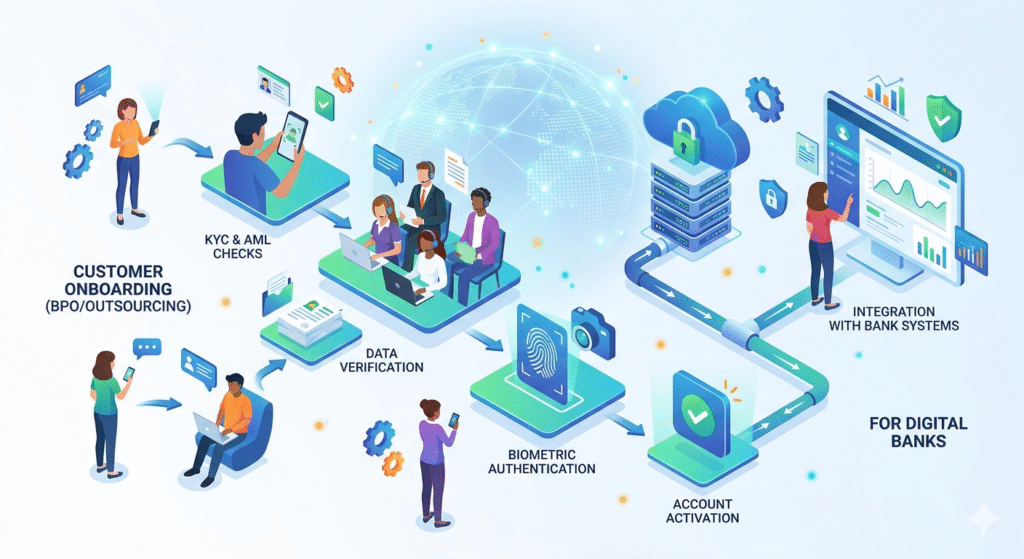

Key Architectural Components

- Identity Verification Hub: Centralized platform integrating multiple identity verification methods (biometric, document-based, database checks) with real-time fraud detection.

- Workflow Orchestration Engine: Configurable rules engine to automate the onboarding journey, adapting dynamically to customer segments, product choices, and regional regulations.

- CRM Integration Layer: Seamless bidirectional data exchange with the bank’s existing CRM systems to ensure a unified customer view and data consistency.

- Compliance and Audit Trail Module: Dedicated subsystem for logging all actions, decisions, and data points, providing an immutable record for regulatory audits.

- Customer Communication Gateway: Automated, multi-channel communication (SMS, email, in-app notifications) for status updates, document requests, and approval confirmations.

- API Gateway: Secure, standardized interfaces for integration with third-party data sources, credit bureaus, and payment gateways.

These architectural components collectively form a resilient and extensible framework. Each element plays a distinct role in ensuring data integrity, process efficiency, and regulatory compliance throughout the customer’s initial interaction with the bank.

Key Deployment Challenges

- Legacy System Integration: Bridging the gap between modern outsourced platforms and existing core banking systems without disrupting operations.

- Data Security & Privacy Concerns: Ensuring robust data encryption, access controls, and adherence to data residency requirements, particularly for cross-border operations.

- Regulatory Compliance Mapping: Translating complex and evolving regulatory mandates (e.g., GDPR, DORA, RBI KYC guidelines) into executable workflow rules within the outsourced system.

- Vendor Management & SLA Adherence: Establishing clear service level agreements (SLAs) and robust governance mechanisms to monitor performance, security, and compliance of the outsourcing partner.

- Change Management & User Adoption: Training internal teams and managing the transition from traditional to outsourced processes, ensuring smooth operational continuity.

- Scalability & Performance Bottlenecks: Designing the outsourced architecture to handle anticipated peak loads and prevent performance degradation during high-volume periods.

Addressing these challenges proactively through detailed planning and phased implementation is crucial for mitigating risks and maximizing the return on investment from an outsourced onboarding strategy.

| Capability | Traditional In-House Onboarding | Outsourced AI-Driven Onboarding System |

| Identity Verification | Manual review of documents, fragmented third-party checks. High error rate, slow processing. | Automated biometric analysis, AI-powered document verification, real-time database cross-referencing. 99% accuracy, near-instantaneous. |

| Risk Assessment | Heuristic rules, manual data entry for credit checks. Inconsistent application, prone to bias. | Machine learning models evaluating multiple data points, predictive fraud analytics. Consistent, objective risk scoring, 25% faster resolution of high-risk cases. |

| Compliance Auditing | Periodic, labor-intensive review of sampled cases. Difficult to trace individual decisions. | Immutable audit trails for every decision and interaction, automated compliance checks against dynamic rule sets. Facilitates rapid, comprehensive audits. |

| Scalability | Linear scaling with staffing increases, significant lead time for training. Limited elasticity. | On-demand scalability leveraging cloud infrastructure and shared service models. Handles 30-50% volume fluctuations without operational impact. |

| Cost Per Onboarding | High operational overhead from staffing, infrastructure, and manual error correction. | 30-50% cost reduction due to automation, shared resources, and reduced error rates. |

The comparative analysis highlights a clear shift from labor-intensive, often inconsistent internal processes to an automated, intelligent, and scalable outsourced model. This transition not only drives efficiency but fundamentally redefines the customer experience by reducing friction and accelerating time-to-value for new clients.

Robust Governance and Regulatory Adherence

Effective governance is paramount when outsourcing critical functions like customer onboarding. Digital banks must establish comprehensive oversight mechanisms to ensure continuous compliance with diverse regulatory frameworks such as GDPR for data privacy, DORA for operational resilience, and specific KYC/AML guidelines set by authorities like the RBI. These regulations demand stringent control over customer data, process transparency, and system integrity.

Outsourced solutions incorporate robust audit logs, meticulously recording every step of the onboarding journey, from initial data capture to final account activation. This level of detail provides complete decision traceability, allowing regulators and internal auditors to reconstruct any customer’s application process and verify adherence to policies and legal requirements. Automated checks and balances are built into the workflow, flagging anomalies and ensuring that all necessary compliance steps are completed before progression.

Regular independent audits of the outsourcing partner’s systems and processes are essential. These audits, coupled with detailed reporting on performance against agreed SLAs, provide the digital bank with assurances regarding data security, service availability (e.g., 99% SLA adherence), and continuous regulatory alignment. Such a structured governance model fosters trust and ensures the outsourced function operates within defined risk parameters.

Actionable Scenarios for Outsourced Onboarding

Scenario: Expedited SME Account Opening

Problem: A digital bank targets small and medium-sized enterprises (SMEs) but faces prolonged onboarding times due to complex corporate structure verification and multiple signatory checks. This results in a high drop-off rate, as businesses often need immediate access to banking services.

Implementation: The bank outsources SME onboarding to a specialized provider leveraging AI-driven corporate registry lookups, automated beneficial ownership verification, and integrated digital signature solutions. The platform automates document collection and cross-references data against global corporate databases.

Measurable Outcome: Onboarding time for SME accounts reduced by 40%, with a corresponding 20% increase in successful account activations within the first quarter. Customer satisfaction (CSAT) scores for the SME segment improved by 15% due to the streamlined process.

Scenario: Cross-Border Customer Acquisition Optimization

Problem: A digital bank expands into new international markets, encountering diverse local KYC requirements, language barriers, and fragmented identity verification infrastructures. This complexity impedes rapid market penetration and inflates operational costs.

Implementation: The bank partners with an outsourcing provider offering a global onboarding platform with configurable workflows tailored to specific country regulations. The platform integrates with local identity databases and offers multi-language support, supported by a global network of human verification agents for edge cases.

Measurable Outcome: The bank achieved a 20-40% efficiency improvement in processing international applications and reduced operational costs associated with manual verification by 35%. This enabled market entry into three new territories within six months, significantly faster than internal capabilities would allow. In a recent deployment across a regional lending portfolio, recovery rates improved by 14% within 90 days, underscoring the operational efficiency gains.

Technology Maturity and Enterprise Adoption Timeline

The adoption of outsourced customer onboarding solutions follows a predictable maturity curve for most enterprise digital banks.

Early Stage (6-12 Months): Initial focus involves selecting a vendor and integrating foundational identity verification and compliance modules. This phase often targets high-impact, low-complexity segments or specific geographies. The primary goal is to establish proof of concept, ensure regulatory alignment, and demonstrate early efficiency gains, often beginning with a 20% efficiency improvement in pilot cohorts. Careful data migration and security protocol implementation are critical during this period.

Scaling Phase (12-24 Months): As confidence grows and initial metrics validate the outsourced model, the digital bank expands its scope. This includes integrating more complex workflows, such as multi-product onboarding or specialized customer segments (e.g., high-net-worth individuals, businesses). The focus shifts to optimizing end-to-end customer journeys, leveraging advanced analytics from the outsourcing partner to identify and mitigate drop-off points. Expect to see a 30-50% cost reduction and 15-30% CSAT increase as processes mature.

Future Model (24+ Months): In its fully mature state, outsourced customer onboarding becomes an integral part of the bank’s growth strategy. The focus evolves towards predictive analytics, hyper-personalization of onboarding flows, and continuous process automation powered by AI. The outsourcing partner acts as a strategic extension of the bank’s operational capabilities, collaboratively innovating to preempt regulatory changes and unlock new revenue streams. This stage often includes exploring further AI system integrations for fraud detection, aiming for an additional 10-18% recovery uplift from sophisticated fraud attempts.

Key Takeaways

- Outsourcing customer onboarding for digital banks significantly enhances operational scalability and reduces internal resource strain.

- Advanced architectural components drive efficiency, real-time verification, and robust compliance across the onboarding journey.

- Proactive management of integration complexities, data security, and regulatory mapping is crucial for successful deployment.

- AI-driven outsourcing yields substantial improvements in identity verification accuracy, risk assessment, and auditing capabilities, leading to 30-50% cost reductions.

- Structured governance, including audit logs and decision traceability, ensures continuous regulatory adherence to frameworks like GDPR and DORA.

- Strategic scenarios demonstrate tangible benefits, such as accelerated SME account opening and optimized cross-border acquisition, with measurable outcomes like 40% reduction in onboarding time.

- The adoption timeline progresses from foundational integration to a future model of predictive analytics and strategic innovation.

FAQs

What specific regulations does outsourced onboarding help digital banks comply with?

Outsourced onboarding solutions are designed to align with a wide array of regulations, including KYC/AML guidelines from central banks (e.g., RBI), data privacy mandates like GDPR, and operational resilience frameworks such as DORA. Providers build configurable workflows that adapt to these evolving legal requirements, ensuring continuous compliance.

How does an outsourced solution impact customer drop-off rates?

By streamlining the onboarding process through automation, real-time verification, and intuitive user interfaces, outsourced solutions significantly reduce friction points. This leads to a faster, more seamless experience, which in turn minimizes customer frustration and can reduce drop-off rates by 20-40% compared to traditional methods.

What are the key data security considerations when outsourcing?

Data security is paramount. Digital banks must ensure outsourcing partners adhere to stringent security protocols, including end-to-end encryption, multi-factor authentication, robust access controls, and compliance with data residency laws. Comprehensive data processing agreements and regular security audits are essential components of the vendor relationship.

Can an outsourced onboarding platform integrate with existing core banking systems?

Yes, modern outsourced platforms are built with robust API gateways designed for seamless integration with existing core banking, CRM, and other enterprise systems. This ensures data consistency, avoids silos, and enables a unified view of the customer across all bank operations.

What is the typical return on investment for outsourcing customer onboarding?

The ROI is typically realized through significant cost reductions (30-50% in operational expenditure), increased efficiency (20-40% improvement), higher customer conversion rates, and reduced compliance risks. Faster market entry and improved customer satisfaction also contribute to long-term business growth and profitability.

The strategic decision to embrace outsourcing customer onboarding for digital banks offers a compelling pathway to enhanced operational efficiency, robust compliance, and superior customer experiences. By leveraging specialized external expertise, financial institutions can navigate complex regulatory environments and scale rapidly without compromising security or service quality. This enables a sharper focus on innovation and market differentiation, critical for sustainable growth in the digital banking sector.

If your organisation is evaluating scalable operating models, Outsourcing Customer Onboarding for Digital Banks may warrant a structured review across cost, governance, and long-term operational resilience.

To explore what that could look like in practice, contact SummitNext for a consultative discussion.